Monetary and Nonmonetary Explanations for the Great Depression

The Great Depression was a worldwide event that kicked

off with the stock market crash of October 29, 1929. The general causes for the

crash are understood to be the accumulation of easy credit based on an overly

optimistic financial outlook throughout the 1920s. This trend resulted in risky

credit decisions on the part of banks and other lenders, including loaning

money for marginal investments. The rising debt across the board created market

instability and eventually led to the crash.

The primary economic theories have reached a rough

consensus that world governments were too slow to react to the crash and

subsequent business failures, leaving lenders holding the bag, often with no

way to liquefy what assets they had. It is generally asserted that governments

should have quickly lowered interest rates, lowered taxes, and injected cash

into the system to ease liquidity problems. Most governments either did not

take these actions or waited too long before acting. The theory I will discuss,

as best I can, is the monetarist theory as put forth by Milton Friedman and

Anna J. Schwartz and its extension by Ben Bernanke.

I

must note that I have little to no economic expertise and will, essentially, be

parroting what I have read this week. I will also say that Bernanke’s Nonmonetary Effects of the Financial Crisis in the

Propagation of the Great Depression, outside of the equations, was the

only reading with which I could make any real headway in terms of understanding,

and even then, it resonated because it seemed to make sense, not because I have

anything by which to confirm it. As such, I will lean heavily on Bernanke

within the framework of Friedman and Schwartz. Money and finance have always

baffled me, so I make that qualifier.

Friedman and Schwartz refer to the reduction of money in

the economy between 1930 and 1933 as the “Great Contraction.” As Bernanke

notes, this was part of the banking crisis of that same period. Before the

advent of the Federal Reserve in 1913, bank liquidity problems in times of

panic were controlled by temporarily suspending the convertibility of deposits

into cash. This moderated the effects of bank runs on the liquidity of the

banks themselves. Prior to 1913, this tactic was initiated by clearinghouses,

which were loose organizations of urban banks.

After

1913, the clearinghouses assumed the Federal Reserve would take the

responsibility for the suspensions, and thus for controlling bank runs. As it

turned out, the Federal Reserve did no such thing, resulting in often ruinous

bank runs between 1930 and 1933 as the public’s trust in financial institutions

bottomed out. This had the effect of drastically reducing the money supply that

the economy needed to function. The worst of the banking crisis was stopped by

the Roosevelt Administration’s Bank Holiday of March 1933. Even so, many

smaller banks did not reopen after the holiday.

Bernanke’s

article, while accepting Friedman and Schwartz’s monetary theory, goes on to

discuss nonmonetary reasons for the length and depth of the Depression. The

bank failures coincided with a high rate of bankruptcy and default among

borrowers from top to bottom. Bank runs combined with loan defaults and the

failure of the Federal Reserve to restrict withdrawals to strip banks of their

cash reserves while also limiting their positive cash flow through loan

repayment.

As

lenders dealt with increasing defaults, the cost of credit increased across the

board, making it more difficult for smaller borrowers to secure the financing

they needed for their projects. The lower loan rate meant the loss of experience

and expertise on the part of lenders in evaluating potential borrowers. As the

lenders became less proficient, and therefore less confident, the less willing

they were to extend credit to potentially risky clients. As their income from

loans plummeted, banks turned toward more liquid investments. Thus, fewer

projects led to less cash flow through the economy and a higher unemployment

rate. Tighter credit also meant that credit was more expensive, as the costs of

credit services and interest rates rose. Those who could obtain credit found

themselves allotting far more of their income to debt service. This situation

resulted in borrowers turning to alternate forms of credit, such as trade

credit. As the hold on credit by the banks was reduced, the costs of credit

were increased here too, as the alternate providers were not as efficient and

lacked the traditional resources of the banks.

The

cost of credit was also affected by rising bankruptcies. As the banking crisis

developed, the value of debtors’ collateral decreased, limiting the banks’

ability to recoup the value of defaulted loans, as well as debtors’ ability to

pay the difference once the collateral was taken by the banks. This forced the

banks to write more comprehensive loan agreements, which increased costs while

also restricting credit to only those who could best afford it.

After

the March 1933 Bank Holiday, the Federal Government took a direct hand in all

aspects of the financial system. Bernanke claims that this effort was the only

real success of the New Deal. The damage to the credit markets, however, had

been done. The banks had set their new credit programs and many prospective

borrowers had turned to alternate sources. These trends took several years to

reverse and tight credit and debtor insolvency remained a problem.

I am unsure how to conclude this essay. Friedman and Schwartz argue convincingly for a monetary interpretation for the Great Depression. Bernanke agrees but adds that nonmonetary influences contributed significantly to the length and depth of the Depression. It does appear that, the nosedive of 1938 notwithstanding, the economy was slowly recovering after 1933. It my be that government intervention contributed to that recovery, but it may also be the slow turn back to traditional economic activity after the shocks from 1930 to 1933. Full recovery did not take place until 1942 when US involvement in World War II returned the nation to full employment. While this is undisputed, it muddies the course of the recovery from a purely economic standpoint.

Bernanke, Ben S., “Nonmonetary

Effects of the Financial Crisis in the Propagation of the Great

Depression.” The American Economic Review

Vol.73 No. 3 (June 1983): 257-276. Nonmonetary

Effects of the Financial Crisis in the Propagation of the Great Depression

(liberty.edu).

Rockoff, Hugh, A Monetary History of the United States, 1867-1960, a Review Essay. EH.Net. Search Results a monetary history of the united (eh.net).

“The Great Depression: Overview and Economic Explanations.” Corporate Finance InstituteThe Great Depression - Overview and Main Economic Theories (corporatefinanceinstitute.com).

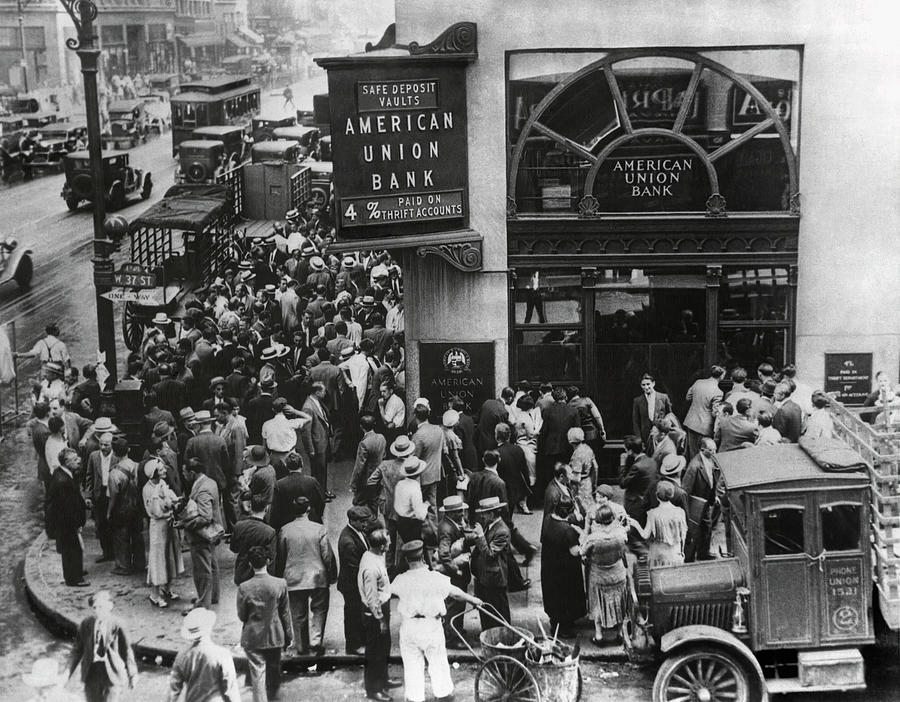

Photo 1: Bank Run, 1931. run-on-bank-great-depression-1931-daniel-hagerman.jpg (900×702) (fineartamerica.com)

Photo 2: Bank Run in San Antonio, Texas, 1931. Run on San Antonio’s City-Central Bank and Trust Company during the Depression, 1931 | Humanities Texas

Photo 3: the Dow Jones through the Great Depression. The Great Depression - Overview and Main Economic Theories (corporatefinanceinstitute.com)

{kind=link}

Comments

Post a Comment